For most Nigerians, buying a home outright is not immediately possible. A mortgage, a loan secured against the property being purchased, is how millions of people in other countries access homeownership. In Nigeria, the mortgage market has historically been underdeveloped, but options do exist, and understanding them could be the difference between owning a home and waiting indefinitely.

This guide breaks down every mortgage option available to first-time buyers in Nigeria, what each requires, and how to decide which path makes sense for your situation.

Leisure Court Editorial Team

Real Estate and Property Development, Nigeria

Leisure Court has been developing affordable residential estates across Abuja, Lagos, Akure and Osogbo for over 7 years. Our team writes to help Nigerian buyers make informed real estate decisions.

What this article covers

The Reality of the Nigerian Mortgage Market

Nigeria's mortgage market is small relative to the size of the economy. Mortgage loans as a percentage of GDP remain below 1%, compared to over 70% in the UK and 50% in South Africa. Interest rates are high, tenors are short, and documentation requirements are demanding.

Despite this, mortgages are available and for buyers who qualify and plan carefully, they represent a structured path to property ownership that is better than delaying indefinitely in the hope of saving a full purchase price while property values continue to rise.

Partnering early with a trusted real estate developer in Nigeria can help you understand which financing route suits your specific situation and what documentation you will need to prepare.

Option 1: National Housing Fund (NHF) Mortgage

The National Housing Fund is a federal government scheme administered by the Federal Mortgage Bank of Nigeria (FMBN). It is the most affordable mortgage option available to employed Nigerians.

How It Works

Employees in both the public and private sectors contribute 2.5% of their monthly basic salary to the NHF. After contributing for a minimum of 6 months, they become eligible to apply for a mortgage through the FMBN or an accredited Primary Mortgage Bank (PMB).

Key Terms

- Interest rate: 6% per annum (fixed) — the lowest available in Nigeria

- Maximum loan amount: ₦15 million (subject to periodic review)

- Maximum tenor: 30 years

- Equity contribution: Minimum 10% of property value

Eligibility Requirements

- Must be a Nigerian citizen aged 21–60

- Must have contributed to NHF for at least 6 months

- Must not have previously benefited from an NHF loan

- Must have a clean credit record

- Must be buying from an FMBN-approved developer or seller

Limitations

The ₦15 million cap is a significant constraint in Lagos and Abuja, where entry-level apartments in decent locations start well above this figure. NHF mortgages are more practical for buyers in Abuja's satellite towns, emerging estates in Osogbo, Akure, and secondary cities where property values are lower.

For more information, visit fmb.gov.ng.

Option 2: Commercial Bank Mortgage

Most of Nigeria's tier-1 banks offer mortgage products for residential property purchase. These are significantly more expensive than NHF loans but cover higher property values and are available to a wider range of buyers.

Key Terms

- Interest rate: 18–26% per annum (variable, Naira-denominated)

- Maximum loan amount: Varies by bank, often up to ₦200 million or more

- Maximum tenor: 5–20 years (varies by bank)

- Equity contribution: Typically 20–30% of property value

Eligibility Requirements

- Verifiable, stable income (salary or business)

- Clean credit record with the Credit Risk Management System (CRMS)

- Property must have a Certificate of Occupancy or equivalent clean title

- Life insurance policy may be required

- The property will be used as collateral

Considerations

The high interest rates of commercial bank mortgages in Naira mean the total cost of borrowing is substantial. On a ₦20 million loan at 22% over 15 years, total repayments will far exceed the original principal. This does not make it a bad option, it depends heavily on your income trajectory, the appreciation potential of the property, and your alternative uses for that capital.

Always use a mortgage calculator and model multiple scenarios before committing.

Option 3: Developer Payment Plans

Many reputable developers in Nigeria offer instalment payment plans that function similarly to a mortgage but without bank involvement. These plans are often the most practical option for buyers who do not qualify for bank financing or do not want to pay bank interest rates.

Typical Structure

- Deposit of 20–30% upon signing the Sale and Purchase Agreement

- Balance spread over 12 to 36 months in agreed instalments

- No interest charged by some developers; others apply a modest carrying fee

- Title transfer occurs on completion of payment

This is particularly common with off-plan properties, where the construction timeline aligns naturally with a payment schedule.

When evaluating a developer payment plan, confirm:

- That the agreement is legally documented with a proper Sale and Purchase Agreement

- That there are clear completion guarantees with penalty clauses if the developer defaults

- That your instalments are held in a designated account (not used for general operations)

- That the title status of the land is verified before you begin paying

A Nigerian real estate developer that operates transparently will provide all of this upfront without being asked.

Option 4: Diaspora Mortgage and Remittance-Backed Purchase

For Nigerians in the diaspora, several banks and developers offer mortgage products denominated in foreign currency (USD or GBP), which removes Naira devaluation risk from the equation.

Key Features

- Loan denominated in USD or GBP

- Repayments made via remittance from abroad

- Lower effective interest rates than Naira mortgages (typically 7–12% in USD terms)

- Requires proof of foreign income, bank statements, and documentation of residency abroad

- Property must have clean title in Nigeria

Some banks with diaspora banking divisions also offer pre-approval processes that can be initiated from abroad before the buyer visits Nigeria for site inspection.

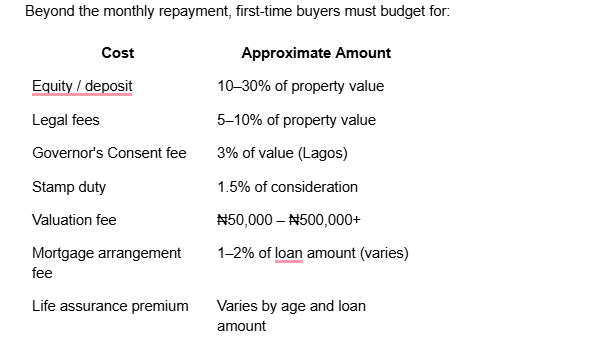

The True Cost of a Mortgage in Nigeria: What to Budget

These costs should all be factored in before you commit to a price or a repayment schedule. A property that seems affordable at the headline price can become a financial strain once all associated costs are included.

Practical Steps for First-Time Buyers Seeking a Mortgage

1. Confirm your NHF contribution status. If you are employed, you are likely already contributing. Contact your employer's payroll department or FMBN directly to verify.

2. Check your credit record. Request your credit report from the Credit Bureau (CRC, First Central, or XDS Credit Bureau) before approaching any lender. Resolve any negative entries before applying.

3. Gather your documentation early. Most mortgage applications require: 6–12 months of bank statements, tax clearance certificates, payslips or business financial statements, a valid ID, and a property valuation report.

4. Get pre-qualified before selecting a property. Knowing how much a bank will lend you before you start viewing properties saves time and prevents the disappointment of falling in love with something outside your financing range.

5. Work with a developer who has banking relationships. Established developers often have pre-existing relationships with mortgage banks and can facilitate faster approvals for their buyers.

Final Word

A mortgage in Nigeria is not impossible, but it requires planning, documentation, and a clear-eyed view of the true cost of borrowing. The most affordable route for most employed Nigerians remains the NHF mortgage; for higher-value properties, commercial bank products and developer payment plans offer viable alternatives.

Whatever route you take, ensure the property itself has clean, verified title, no lender will finance a property with disputed or incomplete documentation.

If you are a first-time buyer looking at properties in Abuja, Lagos, Akure, or Osogbo, speak with the Leisure Court team about payment plan options and which financing route best suits your circumstances.

Related Articles:

- A Buyer's Guide to Top Real Estate in Nigeria

- What to Look for in a Real Estate Developer in Nigeria

- 5 Documents You Must See Before Buying Property in Nigeria

Ready to take the next step in your property journey?

Explore verified projects from Leisure Court or begin your purchase process.

Start nowFrequently asked questions

More in Buyer's Guide

Buyer's Guide

Buyer's GuideBuying in Lekki: What You Need to Know

Lekki is Lagos' most active real estate corridor and one of Nigeria's most misunderstood. Prices range from accessible to extraordinary; titles range from bulletproof to deeply problematic; and the area is developing so fast that decisions made without up-to-date information can be costly.

Read More Buyer's Guide

Buyer's GuideCommercial Real Estate Opportunities in Nigeria 2026

Commercial real estate in Nigeria is frequently overshadowed by the residential market in public conversation, but for informed investors, it offers some of the most compelling yield and appreciation opportunities available in the country.

Read More Buyer's Guide

Buyer's GuideOff-Plan vs Ready-Built Property in Nigeria: Which Is Right For You?

Two buyers with identical budgets can make very different decisions and both be right; if they are buying for the right reasons. Off-plan and ready-built properties represent fundamentally different risk and return profiles.

Read More Buyer's Guide

Buyer's GuideDiaspora Real Estate Investment: Practical Steps

This guide gives you a practical, honest roadmap for navigating the process from wherever you are in the world.

Read More